Many in the anti-monopoly movement are celebrating the recent DOJ victory against the Northeast Alliance (NEA). It’s a rare enforcement action in the airline industry, and a rare decision that gives a clear victory to the DOJ.

But I will not be celebrating. What follows is my attempt to read the potential tea leaves from the NEA decision in looking forward to the JetBlue/Spirit merger. The TLDR: Don’t count the JetBlue/Spirit merger down and out based upon the NEA decision. While I’m pleased with DOJ’s victory, one step forward does not eradicate the giant leaps backward that have befallen the airline industry in the past few decades.

Fake Remedies and Abdication of Responsibility

In every instance of past consolidation in the airline industry, the DOJ (a) did nothing; (b) compelled the divestiture of slots and gates; or (c) filed a complaint, then got spanked by politicians into settling for slots and gates.

A couple of examples should suffice.

In 2013, the DOJ entered into a consent decree in the proposed merger of U.S. Air and American Airlines. The remedy, as is often the case, focused on the sale of slots and gates at LaGuardia Airport, as well as gates at other airports.

Yet the complaint stated that competition would have been enhanced with the emergence from bankruptcy of American Airlines as a standalone competitor. The complaint also argued that the industry had suffered from consolidation (from nine to five majors), and that fares increased due to that consolidation.

So, it’s only natural that slots and gates at a few airports would fix that, right? Not according to the complaint. Head-to-head competition would be eradicated. And it’s hard to start a network carrier, I might add, even with access to slots and gates.

One other example is in order. In the United-Continental merger, despite 18 overlapping markets (routes), the DOJ closed the investigation into the merger with the parties’ agreeing to sell slots and other assets in Newark to Southwest Airlines.

Slots and gates solve all ills in the airline industry. Got it. Unless you’re in one of those overlapping markets, where there is no obligation of the winning bidder of said slot to service the same route. Or unless you’re in rural America, where service has either disappeared completely or is much more expensive.

I don’t want to rehash the entire history of consolidation in the airline industry or the significant role that DOJ has played in shaping that development, but these two transactions are just a few on the path of placating the airlines by essentially creating a “tax” on the transaction that did not cure the anticompetitive ills of the mergers whatsoever. I do not, by the way, blame my former colleagues on staff at the DOJ for this. My blame goes higher up than the trial attorneys and paralegals who work those cases.

Given these data points, does the decision by Judge Sorokin represents a “sea change” in antitrust enforcement in the airline industry? I think not. Let’s break the decision down by some key elements: Concentration, efficiencies, and entry. I’ll also add a comment about the role of economists in that analysis.

Concentration Is Not New

Judge Sorokin discovered what many of us know already: “The industry is highly concentrated. Four carriers control more than eighty percent of the market for domestic air travel: the three GNCs (American, Delta, and United) and Southwest. The remainder of the market—less than twenty percent—is generally split among nine smaller carriers.”

At mainstream antitrust conferences, where consultants are rewarded for taking positions aligned with the most powerful, one might find a variety of people telling you that the airline industry is not concentrated. Since 2001, American bought TWA, U.S. Airways bought America West, American merged with U.S. Air, Delta with Northwest, United with Continental, and Southwest with AirTran. The full list can be found here. In each instance, DOJ was complicit. And, by the way, the market was highly concentrated before those decisions. Take DOJ’s complaint in U.S Air/American: “In 2005, there were nine major airlines. If this merger were approved, there would be only four. The three remaining legacy airlines and Southwest would account for over 80% of the domestic scheduled passenger service market, with the new American becoming the biggest airline in the world.” Indeed, many of the HHIs in the markets in question in that merger exceeded 2,500, or what the Merger Guidelines consider to be “highly concentrated markets.”

After that merger, others followed. Alaska and Virgin merged, Southwest bought some locals, and United bought ExpressJet.

So it is only natural that the DOJ allege concentrated markets in its complaint in the JetBlue/Spirit Merger: According to the agency’s calculations, the merger increases concentration in 150 routes, including 40 nonstop routes. The complaint alleges the risk of heightened coordination among the remaining airlines as well and lower innovation in service.

In short, there is nothing new on the concentration side. ‘Twas ever thus (at least the past 20 years). This suggests that high concentration is not predictive of stopping an anticompetitive merger.

Efficiencies Arising from the Elimination of Competition

Judge Sorokin was skeptical of the claimed efficiencies in the NEA: “American’s Chief Executive Officer (‘CEO’) described the numerous challenges created by mergers, as well as the “inordinate amount of management time and attention” required to integrate two airlines.” Prior mergers touted those great efficiencies. Some during that time period (me included) argued that those efficiencies do not pan out, take longer to achieve, and may be ethereal.

But the parties to the NEA claimed efficiencies even absent merger. Judge Sorokin rejected the claimed efficiencies, ruling they were insufficient to rebut the claimed harms in the NEA litigation. As Judge Sorokin pointed out: “These features arise only if the defendants mimic one carrier, elect not to compete with one another, and cooperate in ways that horizontal competitors normally would not. This elimination of competition negatively impacts the number and diversity of choices available to consumers in the northeast. As such, ‘benefits’ arising in this way cannot justify the defendants’ collusion.”

It’s hard to read that conclusion without thinking about the claims of merger efficiencies in the past. It suggests that the efficiency claim would have been stronger if the NEA members had merged rather than formed an alliance. If that’s the right reading, that could spell trouble for the DOJ in JetBlue/Spirit.

So again, nothing new here, except it was defendants arguing that merger efficiencies are hard to achieve, and in essence claimed that the NEA achieved the same efficiencies without requiring integration. Again, the U.S. Air/American complaint was skeptical of such purported efficiencies: “There are not sufficient acquisition-specific and cognizable efficiencies that would be passed through to U.S. consumers to rebut the presumption that competition and consumers would likely be harmed by this merger.”

Often times, those statements are made in hopes of “out of market” efficiencies counting in favor of the transaction. As the Commentary to the Merger Guidelines states, “Inextricably linked out-of-market efficiencies, however, can cause the Agencies, in their discretion, not to challenge mergers that would be challenged absent the efficiencies. This circumstance may arise, for example, if a merger presents large procompetitive benefits in a large market and a small anticompetitive problem in another, smaller market.” While that Commentary goes against everything that Philadelphia National Bank stands for, it is nonetheless continued policy. Just ignore the citation to Philadelphia National Bank in the complaint. That’s on presumptions.

Nonetheless, the complaint in Jet Blue/Spirit states that “Defendants have not yet described any procompetitive efficiencies in the alleged relevant markets.”

The American Antitrust Institute has been shouting this point for at least a decade. Take Diana Moss’s paper in 2013, explaining that: “System integration (e.g., integrating reservation and IT systems and combining workforces) in some past mergers has been difficult, protracted, and more costly than what was predicted by the airlines.” Others, including yours truly, have asserted the same.

Entry Is Not Easy

Judge Sorokin indicates that barriers to entry into the markets where NEA operates are significant, with likely entry not mitigating the anticompetitive effects. For example, in Boston and New York City, the judge describes the entry barriers as insurmountable: “By ending competition between American and JetBlue, the NEA means that seventy-three percent of domestic flights at Logan are controlled by two (rather than three) entities: Delta and the NEA. In New York, where entry or expansion by any airline is severely limited due to the FAA’s slot constraints at JFK and LaGuardia, the NEA ensures that eighty-four percent of the slots at JFK and LaGuardia are held by the same two (rather than three) entities that now dominate Logan.”

The JetBlue/Spirit complaint concurs: “New entrants into airline markets face significant barriers, including: difficulty in obtaining access to airport facilities or landing rights, particularly at congested airports; existing loyalty to particular airlines; and the risk of aggressive responses to new entry by a dominant incumbent.”

Curious. If entry is as difficult as the current DOJ and Judge Sorokin now suggest, where were those concerns in the prior two decades, when gate and slot sales were held out as the great elixir to lost actual competition?

Not All Economists

Judge Sorokin found defendant economists’ testimony problematic, lacking in nuance, and biased: “The apparent bias of the defendants’ retained experts is reason enough to reject the

opinions and conclusions they rendered in this case.” Again, this is not a surprise. Matt Stoller’s description of people in lab coats who never get graded on their assignments is apt.

Much has been written about the repeated use of economists to weave magical models that later result in unhappiness for consumers. ProPublica had a piece on the expert economist market four years ago, titled “These Professors Make More Than A Thousand Bucks an Hour Peddling Mega Mergers.” The title is a bit dated, due to the inflationary effects in the economic expert market—$1,000 is considered affordable now. Regardless, this practice is ages old. Agencies almost expect certain economists to walk in the door peddling particular mergers. I should disclose my own personal experience getting stomped by Dan Rubinfeld as I sought to stop the United/Continental merger. Consolidation in 18 nonstop markets was simply insufficient to be a problem for defendants’ economist, who was far more prepared, diligent, and careful.

I do not take Judge Sorokin’s judgment of defendants’ economists as a judgment of all experts. I take it to mean that economists must do more to shore up their assertions and conclusions apart from merely proclaiming themselves to be gods of knowledge. In other words, experts should not engage in “sweeping assertions,” “unnuanced and poorly reasoned conclusions,” “overly simplistic view[s],” “absurd” reasoning, or other analysis the court finds is entitled to ultimately “no weight.”

In short, maybe courts will start treating defendant’s economic experts like they treat plaintiff’s economic experts. And yes, that means they’ll get the blame for losing, even if it not deserved. It might also mean that JetBlue/Spirit should think about its expert reports carefully, and who gives those reports.

Conclusion

Before I get emails pointing out that policies and administrations change: I know. But those policies have an effect on the law as it is applied. Just as one example, there is no meaningful or substantive judicial review of consent decrees. And thus, when the DOJ became the Surface Transportation Board of the friendly skies (blessing all mergers that came before it), there was no countervailing power to stop it. Those impacts cannot be undone. They are permanent.

So, while I’m happy about Judge Sorokin’s decision, it doesn’t predict the future. The DOJ may very well still lose JetBlue/Spirit if it goes to trial. And if does lose, it only has its prior self to blame.

In the last thirty years, the United States has experienced a whirlwind of concentration among food suppliers. This elimination of competition is an urgent problem not only because consumers are faced with higher prices and less food choices in grocery stores, but also because the largest agribusinesses on Earth (“Big Ag”), as a result of their massive economic and political power, clog up the workings of our political system to the detriment of democracy and the planet.

Big Ag’s rising profits have been shown to be a driving force behind inflationary food prices again and again. A recent analysis by the White House explained that “If rising input costs were driving rising meat prices, those profit margins would be roughly flat, because higher prices would be offset by the higher costs.”

In addition to these already egregious displays of power and control, Big Ag also destroys the planet’s natural resources, violates existing labor laws, engages in atrocious and inhumane animal processing practices, and puts small farms out of business. Both the legal and economic arrangements that enable this behavior create an unfair political economy that’s immensely profitable and partial to large agribusinesses; these forces allow massive corporations like Monsanto, Tyson, Cargill, and John Deere to largely evade antitrust scrutiny.

As a result, Big Ag players garner enormous market power and uneven political clout, positioning themselves to create even more favorable legislation with which to entrench their dominance in each sector of agriculture, from beef to farming equipment to poultry to seeds.

It Begins on the Farm

An immediate example of Big Ag’s might is in farming equipment. Before the 1930s, over 160 companies sold farm equipment in response to growing industrialization and mechanization of farming. Through industry consolidation, however, John Deere emerged as the leading supplier of agricultural machinery in the United States. Today, John Deere stands alone as the dominant player, commanding roughly 53 percent of the market for large tractors and 60 percent for combines. From 2005 to 2018, John Deere acquired a staggering twelve companies that specialized in sectors ranging from farm equipment to precision technology.

In February, the Department of Justice filed six lawsuits in an effort to crack down on Deere’s monopoly power, engaging in a right-to-repair battle in four states. The lawsuits allege that Deere has illegally attempted to control the repair of Deere equipment, such as tractors and combines, using electronic-control units. The filing contends that the farming equipment giant and its dealerships monopolize the market for repair and maintenance services by designing proprietary Deere equipment, which requires Deere-controlled software for the diagnosis and maintenance functions. That software is exclusively available to technicians authorized by Deere. This arrangement leaves many independent shops and farmers beholden to Deere-authorized vendors when repairing their equipment. In this way, Big Ag poses a sort of private tyranny over those who have to rely on their equipment to make a living, and they are largely left unaccountable to the public and consumers.

Merger Mania

The tentacles of Big Ag reach beyond equipment into our milk and meat supply. Industry concentration in dairy has led to fewer farms and more mega-dairy operations, diminishing the profits of small family farms. The beef industry similarly has become more heavily concentrated. Today, only four firms—Tyson, Cargill, JBS, and National Beef Packing Co.—control over 70 percent of the nation’s beef supply, and they processed roughly 85 percent of cattle in the United States in 2018.

The level of concentration occurred at such a breakneck pace since the 1980s that Department of Agriculture economists characterized this wave of mergers as “merger mania,” during which concentration soared from 35.7% in 1980 to 71.6% by 1990 in the beef packing sector.

For instance, through mergers in the agriculture industry, “the four largest meatpackers have increased their share of the market from 36% to 85%, and the largest four sellers of corn seed accounted for 85% of U.S. corn seed sales in 2015, up from 60% in 2000.

Due to the resulting power over consumers and input providers, these mega-corporations are doing better than ever. The level of concentration, and the control over factory farming that it grants, are partially responsible for Tyson Foods’ beef sales jumping to $5 billion in the first quarter of 2022, lifting overall sales to $12.93 billion. Tyson Foods realized over a billion dollars in new dividends and stock buybacks. Add this to the more than $3 billion already they paid out to shareholders since the pandemic. In beef processing, corporate profits skyrocketed by $96.9 billion in the third quarter of 2021 alone.

Economic Power Translates into Political Power

Though it is hard to pinpoint a specific and clear approximation of the political power large agribusiness has achieved, each industry as a whole has immense political power resulting from their economic growth and profits from concentration. This is malfeasance in the highest order. Food monopolists and other dominant players in our agriculture system have the ability to contribute a large amount of campaign funds to key lawmakers in charge of legislating the sectors where mega corporations have a direct interest.

Farm subsidies in the United States largely support private associations and large corporations. These subsidies account for roughly 39 percent of farm income while the biggest agriculture firms continue to make record-breaking profits. The United States government gives away free money to private corporations that continue to increase their profits without contributing back into the public coffers or without providing adequate care to farm animals or adequate compensation (or safety) to the labor that generates the profit.

One example is the National Cattlemen’s Beef Association (NCBA). Researchers have long understood how clear the intent to monopolize is through the political clout of large, private trade associations, like the NCBA, which is directly paid a proportion of the proceeds from the U.S. government from every beef sale (like supermarkets steaks or hamburgers from a fast-food restaurant). In addition to lobbying for the further consolidation of the meat-processing industry, the NCBA uses these proceeds to lobby for Americans to eat more meat and to oppose district court judges who are sympathetic to animal rights.

The Social Costs Are Adding Up

Food production and industrial farming pose existential threats to critical ecosystems and rural populations, accelerating climate change by polluting and contributing massively to greenhouse gasses. The natural resources needed to sustain the increasing industrialization of our agricultural infrastructure are exhausted at the behest of large industry titans not in the least bit compelled to employ sustainable environmental practices. These effects are undesirable to everyone but to large agribusiness polluters, which perversely gain a greater capacity to pollute and contribute to climate change to a meaningful degree as they grow in scale and size.

The broader societal costs of the size, power, and dominance of food monopolies are far reaching. Economic power garnered from consolidating food industries, especially during the ongoing COVID-19 pandemic, yields uneven political influence—where corporations shape laws to get enacted in their favor, which in turn garners them more control of the food system. In the legal system, the problem of agriculture monopolies cannot be adequately dealt with on purely economic grounds either. This is because of the popularized role that economic analysis plays in assessing anticompetitive harm. With its fixation on short-run consumer price effects, the current economic lens cannot fully capture the ways in which Tyson, Bayer, or Monsanto grow their market power. Like other dominant players in industries, major corporations within Big Ag also mold political outcomes in their favor to avoid critical enforcement. They achieve this by influencing the anti-monopoly policies enacted to proscribe and limit their size in the first place, positioning themselves to dictate the terms for which market activity is stimulated.

When applying the law, antitrust courts should abandon the antiquated Chicago School dogma, which naively assumes that markets are self-correcting and that consumer welfare is paramount. When it comes to assessing the true harms of food monopolies and food barons, which undermine the rights of local farming operations, antitrust authorities should instead consider a broader set of anti-monopoly goals in order to disperse power more evenly among local farming operations nationwide.

To continue to permit consolidation in the aforementioned ways is anti-democratic. A strategy to implement these tools simply requires the political will to hold Big Ag corporate titans accountable by legally compelling them to relinquish control of their hordes of wealth, industry control, and attendant political influence.

Tyler Clark is an economist working on anti-monopoly, corporate power, and antitrust research. A recent graduate of the M.S. program in economics at the University of Utah, Tyler hopes to return and pursue a JD specializing in antitrust law. You can follow him on Twitter @traptamagotchi.

Just weeks after a series of high profile train derailments headlined by the disaster in East Palestine, Ohio, the Surface Transportation Board (STB) decided to double down on the current railroad oligopoly. The STB approved a merger between Canadian Pacific Railway and Kansas City Southern Railway Company, cutting the number of major “Class I” rail companies in the United States from seven down to six. This decision is diametrically opposed to the public interest and seriously undermines trust in rail regulators.

The merger approval clearly violates President Biden’s Executive Order on Promoting Competition in the American Economy, which explicitly directed the STB to begin rulemaking to make it harder for railroads to engage in anticompetitive practices. The order instructed the chair to “consider rulemakings pertaining to any other relevant matter of competitive access, including bottleneck rates, interchange commitments, or other matters.” Instead, the STB has abetted concentration that makes it harder to regulate.

Because the decision goes against Biden’s overarching competition agenda, the Revolving Door Project today released a letter with RootsAction and FreedomBLOC calling for President Biden to relieve Martin Oberman from his chairmanship at the STB. This backtracking requires a major course correction that can only be achieved by a change in leadership.

Besides being antithetical to one of the defining policies of the Biden administration, the STB’s decision breaks from other parts of the administration. As the FTC and DOJ Antitrust Division have redoubled their efforts to push back on monopolization across the economy, the STB approved the first big freight-rail merger since the 1990s. But it’s not just the FTC and DOJ going in the opposite direction of the STB; Secretary Pete Buttigieg and his Department of Transportation have recently raised their scrutiny of transportation mergers, highlighted by blocking airline consolidation.

And while Buttigieg has not explicitly chimed in on the rail merger, other regulators did, warning the STB against approval. The DOJ Antitrust Division warned against the merger, saying it could “empower the merged railroad to deny shippers access to the lowest cost or fastest end-to-end routings. […] The railroad sector in particular, with its relatively high fixed and sunk costs, often enjoys substantial structural entry barriers and advantages that may facilitate or incentivize anticompetitive behavior.”

Additionally, a majority of the Federal Maritime Commission opposed the merger, arguing that “the proposed consolidation does not ensure that the anticompetitive effects of the transaction outweigh the public interest in meeting significant needs.” As I’ve written before, the FMC has a history of serious dovishness on consolidation, making such a strong position all the more notable. The merger is even being opposed by another railroad; Union Pacific is suing to block the STB’s decision.

Besides undermining the administration’s broader policy agenda, the STB’s decision will also undermine safety in the rail industry. What’s the basis for such a strong claim? The STB’s own analysis found the merger would “slightly increase” risks of derailments. Taking their analysis at its word, even slight increases in such risks seem folly after Norfolk Southern set East Palestine ablaze with a single derailment. That incident highlighted how underequipped and unprepared regulators were to deal with any derailment. Allowing an increase in that risk just to enable more corporate profits is a bad trade for the American people.

Another cost of the merger is less effective oversight. As I wrote in The Sling in March, “More industry concentration makes effective regulation harder. As firms increase in size, they gain more and more of a resource advantage over their regulators. One behemoth corporation can often hire more lawyers and cultivate more relationships with lawmakers in order to obfuscate enforcement measures than multiple smaller ones could.”

Of course, there are corporate-friendly defenders of the merger. The Economist argued that the merger “may end up enhancing competition” because the two rail companies do not directly compete—there are no overlapping tracks—and because the merged entity “will provide the first train lines running from Canadian ports through the heart of the United States into Mexico. This is poppycock: A merger that doesn’t involve head-to-head competitors can still be harmful if it enables the merged firm to engage in anticompetitive behavior such as blocking rival’s market access.

Indeed, The Economist gives the game away in the very next paragraph, admitting the rail “industry is also consolidating, which leads to greater pricing power.” There’s only one consolidation going on and it’s the one they’re seeking to defend. If pricing power will increase simply by virtue of consolidation, that means that even though the current lines don’t overlap, the merger facilitates anti-competitive behavior. Full stop.

This is exactly the point the DOJ made in its statement to the STB as well. As they put it:

Even beyond the elimination of head-to-head competition, mergers that increase market power can harm competition in several ways. The merger can empower the merged railroad to deny shippers access to the lowest cost or fastest end-to-end routings. Likewise, in the absence of a complete refusal to interchange traffic, mergers may enable firms to foreclose competition in other ways, such as raising costs for their rivals through control over inputs or access. Such mergers also can create a more conducive structure for post-merger coordination between direct competitors by facilitating communication or discipline through the new integrated asset. The railroad sector in particular, with its relatively high fixed and sunk costs, often enjoys substantial structural entry barriers and advantages that may facilitate or incentivize anticompetitive behavior. For example, railroads may anticompetitively refuse to interchange traffic and/or favor the newly integrated company’s long-haul route over a more efficient joint line route.

Four of the other five Class I railroads agree, having opposed the merger because of how it would enable the new CPKC to block competitors from accessing important junctions, particularly Houston. This comes after earlier concerns from Union Pacific and BNSF around the Houston terminal. In short, the massive market power the merger grants CPKS will allow for the firm to undermine competition by blocking other railroads from readily accessing interchanges and other rail that Kansas City Southern currently shares with other shippers. Despite the two firms not directly competing in their current routes, the vertical integration creates the opportunity to force business away from other railroads because of the degree of control over their competitors’ ability to operate competing routes.

The Canadian Pacific-Kansas City Southern merger undermines administration policy and directly contributes to further anticompetitive practices in the rail industry. It is also likely to cause worse service, job cuts, weaker oversight, and higher prices, among other harms. President Biden should heed his Transportation Department, Justice Department, and Federal Maritime Commission and appoint new leadership at the STB.

Dylan Gyauch-Lewis is a researcher at the Revolving Door Project.

Paradigm change is hard. It took over a year to overcome significant ridicule from neoliberal economists and pundits for the evidence to be so compelling as to flip the consensus on the causes of inflation. Business press outlets from the Wall Street Journal to Bloomberg to Business Insider now perceive what some heterodox economists have recognized for a while—that companies in concentrated industries were exploiting an inflationary environment to hike prices in excess of any cost increases they were incurring. (Alas, The Economist refuses to see the light.) Even Biden’s director of the National Economic Council, Lael Brainard, refers to this bout of inflation as a “price-price spiral, whereby final prices have risen by more than the increases in input prices.”

It’s hard to assign credit for flipping the script, but a few brave economists deserve mention. Isabella Weber, an economist at the University of Massachusetts, published a provocative article, co-authored with Evan Wasner, titled “Sellers’ Inflation, Profits and Conflict: Why Can Large Firms Hike Prices in an Emergency?” They explain how firms with market power only engage in price hikes if they expect their competitors to follow, which requires an implicit agreement that can be coordinated by sector-wide cost shocks and supply bottlenecks.

Josh Bivens of Economic Policy Institute debunked the neoliberal claim that wage demand was driving inflation, showing instead that corporate profit was responsible for more than one third of the price growth. Mike Konzcal and Niko Lusiani of the Roosevelt Institute demonstrated that U.S. firms that increased markups in 2021 the most were those with the higher mark-ups prior to the economic shocks, an indication that concentration was facilitating coordination. (If one were to expand the list of thought influencers beyond economists, you’d have to start with Lindsay Owens of the Groundwork Collaborative, who has been analyzing what CEOs say on earnings calls since the onset of inflation.)

With the new consensus, we need think creatively about attacking inflation. We have more than one tool at our disposal. Rate hikes might ultimately slow inflation, but at enormous social costs, as that mechanism requires putting people out of work so they have less money to spend. What’s worse, rate hikes are regressive, with the most vulnerable among us bearing the largest costs. Solving the inflationary puzzle calls for a scalpel not a chainsaw: We need to identify the industries that contribute the most to inflation (e.g. rental, electricity, certain foods), and then tailor remedies that attack inflation at its source. To use one analogy, it wouldn’t make sense to bulldoze a house because a fire was burning in one room. You’d find that room and put out the fire. I am calling for seven policies in particular.

(1) More Bully Pulpit. The President should use the bully pulpit more—recall JFK’s turning back steel price hikes in 1962. Biden called out junk fees in his state of the union address, causing airlines to remove unwarranted fees for families sitting together. Clearly, Biden can’t hold a press conference about a misbehaving industry daily. But he has not come close to tapping this well.

(2) More Congressional Hearings. Congress should hold hearings to call executives to account for price gouging. Although Congress has held hearings with experts, they have yet to summon the CEOs of industries employing massive price hikes, seemingly in coordination—as if they were some tacit agreement to raise prices in unison. I’d start by calling the CEOs of the packaged food makers, PepsiCo, Unilever, and Nestlé, who bragged last week to investors about record profits, massive price hikes, and enduring pricing power.

(3) The FTC to the Rescue. The FTC should investigate firms for announcing current or future price hikes (or capacity reductions) during earnings calls under the agency’s unique Section 5 authority to police “invitations to collude.” These cases of “tacit collusion” are much harder to prosecute under the Sherman Act. If the FTC were to publicly announce an investigation into a firm or industry—airlines (admittedly outside the FTC’s jurisdiction) or retail would be a good place to start—it would force CEOs economywide to exercise more caution about sharing competitively sensitive information on earnings calls.

(4) Limits on Concentrated Holdings: The cost of shelter makes up a significant share of the core CPI. Cities or states should move to limit the holdings of any individual firm within a given census tract. My OECD paper, co-authored with Jacob Linger and Ted Tatos, showed the nexus between rental inflation and concentration in Florida. A natural cap for a single owner would be five or ten percent of all rental properties in a neighborhood. Raising interest rates, our default anti-inflation tool, perversely puts home ownership out of reach of millions of families, driving them to the rental markets, which bids up rental rates, which is one of the primary drivers of inflation.

(5) Price Controls Should Be on the Table. Price controls are the ugly stepsister in economics. But when backed by a public campaign, they have proven to be effective. Congress imposed price caps for insulin copays in the Inflation Reduction Act, but only for those patients covered by Medicare. Insulin makers, beginning with Eli Lilly, saw the writing on the wall, and voluntarily imposed the $35 cap on all patients. So long as caps are sparingly used in mature industries, the standard investment concerns of economists should be mitigated. The lesson from insulin is that the mere talk of price controls can induce an industry to temper their enthusiasm for price hikes.

(6) Government Provisioning. The threat of government provisioning is another lever that may force private industry to behave. To wit, California offered a $50 million contract to makes its own insulin, which coincided with Eli Lilly, Sanofi and Novo Nordisk preemptively reducing their prices. This playbook could be used in other industries where inflation remains stubbornly high. We can anticipate libertarians screaming “socialism,” but if the cost of inaction is more rate hikes and unemployment, I’d take the libertarian jeers any day.

(7) Fix Antitrust Law. Congress should amend the Sherman Act to give the DOJ, state attorneys general, and private enforcers a better shot at policing tacit collusion among firms in concentrated industries. Courts have implicitly adopted the notion that oligopolistic interdependence is just as likely to achieve prices inflated over competitive conditions as agreement, and so “merely” alleging or putting forward evidence of parallel pricing, excess capacity, and artificially inflated prices is insufficient to prove agreement under Section 1. But why should we presume that it is just as easy to maintain artificially inflated prices tacitly than through agreement?

Congress should flip the presumption. In particular, Section 1 of the Sherman Act should be amended so that the following shall create a presumption of agreement: Evidence of parallel pricing accompanied by evidence of (a) inter-firm communications containing competitively sensitive information, or (b) other actions that would be against the unilateral interests of firms not otherwise colluding, or (c) prices exceeding those that would be predicted by fundamentals of supply or demand. Moreover, the Sherman Act should be amended to permit courts to sanction corporate executives who participated in any price-fixing conspiracy upon a guilty verdict, by barring the executives from working in the industries in which they broke the law, either indefinitely or for a period of time.

Industrial organization gatekeepers like to poo-poo the idea of using competition tools to attack inflation, noting that antitrust moves too slowly. This is needlessly pessimistic. It bears noting that none of the seven remedies suggested here involve bringing a traditional antitrust case against a set of firms pursuant to the Sherman Act. The common thread that binds the first six remedies is inducing a short-run shift in industry behavior. A forced divestiture of rental properties over a holding limit would inject downward-pressure on rents in the short run. CEOs don’t want to be called out by the president or called to testify before Congress to explain their record-breaking profits attributable to massive price hikes above any cost increases. A public investigation by the FTC into invitations to collude via earnings calls would also have an immediate effect on CEOs. Nor would CEOs take lightly to being barred for life from an industry for participating in a price-fixing scheme.

The seven interventions outlined here will require an all-of-government approach. Biden should create a task force to carry out these policies and issue an executive order to signal his seriousness to other agencies. There are two paths for Biden’s legacy: Do nothing about inflation and leave it to the Fed to engineer a recession that likely ends his presidency, or grab the reins himself. With the new consensus emerging that profits (and not wage demands) are driving inflation, the time has come to change our approach.

As the frontline against illegal monopolies and deceptive corporate behavior, the Federal Trade Commission (FTC) has a critical role to play in building an economy that works for consumers and small businesses. Since becoming FTC Chair, Lina Khan’s efforts to rein in anti-competitive behavior and protect consumers has been met with fierce resistance from powerful special interests and hostile editorials in the The Wall Street Journal.

Unfortunately, given the FTC’s role in combating unfair corporate behavior, this pushback is to be expected. I should know: I had the privilege of being an FTC commissioner, serving in both the Clinton and Bush administrations. I’ve seen fair, and unfair, criticism targeted at Republican and Democratic FTC chairs alike.

As a commissioner, I served under Chair Tim Muris, who was appointed by George W. Bush and whose aggressive stewardship of the agency resembled in many ways the current leadership of Chair Lina Khan. While at the helm of the FTC, Chair Muris pursued one of the most aggressive regulatory agendas of any Bush-appointed agency heads. His agenda was assisted by his chief of staff, Christine S. Wilson, who went on to be appointed to the FTC by Donald Trump.

Despite this history, Wilson made big news when, as part of her resignation announcement, she attacked Chair Khan’s “honesty and integrity” and accused her of “abuses of government power” and “lawlessness.” This turned many heads in Washington, particularly mine because of how detached this viewpoint was from my prior experience of serving at the FTC under Wilson’s own stewardship of the agency.

In his 2021 Executive Order on Promoting Competition in the American Economy, President Biden acknowledged that “a fair, open, and competitive marketplace has long been a cornerstone of the American economy.” Unfortunately, corporate concentration has grown under both parties for many years, especially in the technology industry. It is fortunate, and past time, to see the White House, the FTC, Department of Justice, and other agencies working to swing back the pendulum and reinvigorate competition in the American economy.

Despite the ongoing crisis of corporate concentration, Ms. Wilson took objection to an antitrust policy statement the FTC adopted in November and to Chair Khan’s statements in favor of strong enforcement. I found this odd having seen up close Ms. Wilson zealously advance Chair Muris’s enforcement agenda. In office, Muris “challenged mergers in markets from ‘ice cream to pickles,’” as the Wall Street Journal once noted, including in the technology industry, where Lina Khan has devoted significant attention.

During his tenure, Muris used the power available to him as Chair on behalf of consumers and for the good of the economy. He evolved the theory behind FTC regulatory authority so he could take new action to protect consumers—like creating the DO NOT CALL registry—over frivolous legal objections by the telecommunications industry. Like Khan, he coordinated with the DOJ to ensure that they were addressing anticompetitive behavior.

Ms. Wilson claims that Chair Khan should have recused herself from a Facebook acquisition case because of opinions she had expressed as a Congressional staffer. But both a federal judge and the full Commission found no basis to these claims of impropriety, and it is clear that Chair Khan had no legal or ethical obligation to recuse in this case. FTC Commissioners including Khan, like judges, are required to set their personal opinions aside and evaluate cases on the merits, and they do. The FTC Ethics Guidelines tells commissioners to ”not work on FTC matters that affect your interests: financial, relational, or organizational.” When it comes to ethics guidelines, it doesn’t get any plainer than that, and Chair Khan’s participation in the case clearly does not violate these guidelines.

In a hyper-partisan environment, Ms. Wilson’s attacks on the FTC’s credibility appear to me as an attempt to slow antitrust enforcement and ultimately obfuscate Chair Khan’s pro-consumer agenda.

The U.S. Chamber of Commerce, which lobbies against pro-consumer regulations, sent an open letter to Senate oversight committees demanding an investigation of “mismanagement” at the FTC, including congressional hearings. No wonder the Chamber is upset. The Biden Administration is taking the crisis of corporate concentration seriously and is taking steps to bolster antitrust and consumer protection enforcement. That’s a development American consumers should cheer, because when corporate consolidation rises, competition is inevitably diminished, leading to higher prices and fewer choices for consumers.

Fortunately, Chair Khan is building on the legacy of strong leaders like Muris to build an economy that works for consumers, not harmful monopolies. Ultimately, she will be remembered for that and not cynical, distracting attacks on her.

Sheila Foster Anthony, a FTC commissioner from 1997-2003, previously served as Assistant Attorney General for Legislation at the U.S.Department of Justice. Prior to her government service, she practiced intellectual property law in a D.C. firm.

Over the last 40 years, antitrust cases have been increasingly onerous and costly to litigate, yet if plaintiffs can prevail on one single issue, they dramatically enhance their chances of obtaining a favorable judgment. That issue is market definition.

Market definition is straightforward to explain because it’s just what it sounds like. Litigants and judges must be able to delineate the market in question in order to determine how much control a corporation exercises over it. Defining a relevant market essentially answers, depending on the conduct courts are analyzing, whether computers that run Apple’s MacOS operating system or Microsoft Windows are in the same market or, similarly, if Coca-Cola competes with Pepsi.

A corporation’s degree of control over any particular market is then typically measured by how much market share it has. In antitrust litigation, calculating a firm’s market share is the simplest and most common way to determine a firm’s ability to adversely affect market competition, including its influence over output, prices, or the entry of new firms. While the issue may seem mundane and even somewhat technocratic, defining a relevant market is the single most important determination in antitrust litigation. Indeed, many antitrust violations turn on whether a defendant has a high market share in the relevant market.

Market definition is a throughline in antitrust litigation. All violations that require a rule of reason analysis under Section 1 of the Sherman Act, such as resale price maintenance and vertical territorial restraints, require a market to be defined. All claims under Section 2 of the Sherman Act require a relevant market. And all claims under Sections 3 and 7 of the Clayton Act require a relevant market to be defined.

Defining relevant markets stems from the language of the antitrust laws. Section 2 of the Sherman Act states that monopolization tactics are illegal in “any part of the trade or commerce[.]” Sections 3 and Section 7 prohibit exclusive deals and tyings involving commodities and mergers, respectively in “any line of commerce or…in any section of the country[.]” “[A]ny” “part” or “line of commerce” inherently requires some description of a market that is at issue.

As I more thoroughly described in a newly released working paper, the process of defining relevant markets has a long and winding history stemming from the inception of the Sherman Act in 1890. Between 1890 and 1944, the Supreme Court took a highly generalized approach, requiring as it stated in 1895, only a description of “some considerable portion, of a particular kind of merchandise or commodity[.]” In subsequent cases during this initial era, the Supreme Court provided little additional guidance, maintaining that litigants merely needed to provide a generalized description of “any one of the classes of things forming a part of interstate or foreign commerce.”

In 1945, after Circuit Court Judge Learned Hand found the Aluminum Company of America (commonly known as ALCOA) liable for monopolization in a landmark case, the market definition process started to become more refined, primarily focusing on how products were similar and interchangeable such that they performed comparable functions. At the same time market definition took on more complexity, antitrust enforcement exploded and courts became flooded with antitrust litigation. Given the circumstances, the Supreme Court felt that it needed to provide litigants with more structure to the antitrust laws, not only to effectuate Congress’s intent of protecting freedom of economic opportunity and preventing dominant corporations from using unfair business practices to succeed, but also to assist judges in determining whether a violation occurred. Throughout the 1940s and 1950s, the Supreme Court repeatedly expressed its frustration that there was no formal process for litigants to help the courts define markets.

It took until 1962 for the Supreme Court to comprehensively determine how markets should be defined and bring some much-needed structure to antitrust enforcement. The process, known as the Brown Shoe methodology after the 1962 case, requires litigants to present information to a reviewing court that describes the “nature of the commercial entities involved and by the nature of the competition [firms] face…[based on] trade realit[ies].” With this information, judges are required to engage in a heavy review of the information they are presented with and make a reasonable decision that accurately reflects the actual market competition between the products and services at issue in the litigation.

Constructing a relevant market for the purposes of antitrust litigation using the Brown Shoe methodology can be made using a variety of commonly understood and accessible information sources. For example, previous markets in antitrust litigation have been constructed from reviewing consumer preferences, consumer surveys, comparing the functional capabilities of products, the uniqueness of the buyers or production facilities, or trade association data. In a series of cases between 1962 to the present, the Supreme Court has rigorously refined its Brown Shoe process to ensure both litigants and judges had sufficient guidance to define markets. Critically, in no way did the Supreme Court intend for its Brown Shoe methodology to restrict or hinder the enforcement of the antitrust laws, and the fact that the process relies on readily accessible and commonly understood information is indicative of that goal.

But 1982 was a watershed year. Enforcement officials in the Reagan administration tossed aside more than a decade of carefully crafted jurisprudence from the Supreme Court in favor of complex, unnecessary, and arbitrary tests to define a relevant market. The new test, known as the hypothetical monopolist test (HMT), which is often informed by econometric models, asks whether a hypothetical monopolist of the products under consideration could profitably raise prices over competitive levels. It is tantamount to asking how many angels can dance on the head of a pin. They primarily accomplished this economics-laden burden through the implementation of a new set of guidelines that detailed how the Department of Justice would analyze mergers, determine whether to bring an enforcement action, and how the agency would conduct certain parts of antitrust litigation, one of those aspects being the market definition process.

From the 1982 implementation of new merger guidelines to the present, judges and litigants, predominantly federal enforcers, have ignored the Brown Shoe methodology and instead have embraced the HMT and its navel-gazing estimation of angels. As a result, courts now entertain battles of econometric experts, over what should amount to a straightforward inquiry.

As scholar Louis Schwartz aptly described, the relegation of the Brown Shoe methodology and its brazen replacement with econometrics under the 1982 guidelines represented a “legal smuggling” of byzantine economic criteria into antitrust litigation.

Besides facilitating the de-economization of antitrust enforcement, abandoning the econometric process would have other notable benefits. First, relying entirely on the Brown Shoe methodology would restrict the power of judges, lawyers, and economists by making the law more comprehensible to litigants. Giving power back to litigants would contribute to making antitrust law less technocratic and abstruse and more democratically accountable. For example, in some cases, economists have great difficulty explaining their findings to judges in intelligible terms. In extreme cases, judges are required to hire their own economic experts just to decipher the material presented by the litigants. Simply stated, the law is not just for economists, judges, or lawyers; it is also for ordinary people. Discarding the econometric tests for market definition facilitates not only the understanding of antitrust law, but also how to stay within its boundaries.

Second, reverting to the Brown Shoe methodology would make antitrust law fairer and promote its enforcement. The only parties that stand to gain from employing econometric tests are the economists conducting the analysis, the lawyers defending large corporations, and corporations who wish to be shielded from the antitrust laws. Frequently charging more than a $1,000 dollars an hour, economists are also extraordinarily expensive for litigants to employ, creating an exceptionally high barrier to otherwise meritorious legal claims.

Since 1982, market definition in antitrust litigation has lingered in a highly nebulous environment, where both the econometric tests informing the HMT and the Brown Shoe methodology co-exist but with only the Brown Shoe methodology having explicit approval by the Supreme Court. Even in its highly contentious and confusing 2018 ruling in Ohio v. American Express, the Supreme Court did not mention or cite the econometric processes currently employed by courts and detailed in the merger guidelines to define relevant markets. In fact, in a brief statement, the Court reaffirmed the controlling process it developed in Brown Shoe, yet lower courts continue to cite the failure of plaintiffs to meet the requirements of the econometric market definition process as one of the primary reasons to dismiss antitrust cases. Putting it aptly, Professor Jonathan Baker has stated that the “outcome of more [antitrust] cases has surely turned on market definition than on any other substantive issue.”

While the econometric process is not the exclusive process enforcers use to define markets in antitrust litigation and is often used in conjunction with the Brown Shoe methodology, completely abandoning it is critical to de-economizing antitrust law more generally. Since the late 1970s, primarily due to the work published by Robert Bork and other Chicago School adherents, economics and economic thinking more generally have become deeply entrenched in antitrust litigation. Chicago School thought has essentially made antitrust enforcement of nearly all vertical restraints like territorial limitations per se legal, and since the 1970s, the Supreme Court has overturned many of its per se rules. Contravening controlling case law on vertical mergers, Chicago School thinking has resulted in judges viewing them as almost always benign or even beneficial and failing to condemn them by applying the antitrust laws. Dubious economic assumptions have significantly restricted antitrust liability for predatory pricing, a practice described by the Supreme Court in 1986 as “rarely tried, and even more rarely successful.” As a result, economic thinking and econometric methodologies, though running contrary to Congress’s intent, have served to undermine the enforcement of the antitrust laws. This is not to say there is no role for economists. Economists can engage in essential fact gathering activities or provide scholarly perspective on empirical data that shows how specific business conduct can adversely affect prices, output, consumer choice, or innovation. For example, economic research has found that mergers and acquisitions habitually lead to higher prices and increased corporate profit margins – repudiating the idea that mergers are beneficial for consumers. But economists have little value to add when it comes to market definition.

Reinstituting many of the overturned per se antitrust rules all but require a change of precedent from the Supreme Court, which appears highly unlikely given the ideology of most of the current justices. However, modifying the process that enforcers use to determine relevant markets does not require overcoming such a seemingly insurmountable hurdle. Ridding antitrust litigation of the econometric process would simply require enforcers, particularly those at the Federal Trade Commission and the Department of Justice, to completely abandon the process altogether in their enforcement efforts (particularly in the merger guidelines) and instead exclusively rely on the Brown Shoe methodology. Neither the law nor the jurisprudence would need to be modified to effectuate this change—although it might be helpful, before unilaterally disarming, to first explain the new policy in the agencies’ forthcoming revision to the merger guidelines.

While some judges currently ignore or dismiss the Brown Shoe methodology, were enforcers to completely abandon the econometric process for defining markets, courts effectively would have no choice but to rely on the controlling Brown Shoe process. Unlike other aspects of antitrust law, enforcement officials can and should fully embrace the controlling law, in this case Brown Shoe, and use it readily, leaving private litigants to employ the econometric process if they so chose. Nevertheless, history indicates that courts are highly deferential to the methods used by federal enforcers—especially when explicated in the merger guidelines—and private litigants would likely follow the lead of federal enforcers in deciding which method to use to define relevant markets.

Currently, the Department of Justice and the Federal Trade Commission are redoing and updating their merger guidelines. To continue facilitating the progressive antitrust policy that began with President Biden’s administration and to start broadly de-economizing antitrust litigation, both agencies should seize the opportunity to jettison the econometric-heavy market definition tests and enshrine this change within the updated merger guidelines. Enforcers should instead exclusively rely on the sensible, practical, and fair approach the Supreme Court developed in Brown Shoe.

—

Daniel A. Hanley is a Senior Legal Analyst at the Open Markets Institute. You can follow him on Mastodon @danielhanley@mastodon.social or on Twitter @danielahanley.

From its unquestioned bailout of the venture capitalists that ultimately crashed Silicon Valley Bank, to the funneling of public dollars to corporations that shamelessly bribe public officials, the Biden Administration is developing a track record of empathizing with monopolists to whom empathy is utterly unwarranted. It’s not too late to change course.

In January, Congressional Democrats urged Biden’s Secretary of Agriculture, Tom Vilsack, to bar JBS, a food processing company, from U.S. Department of Agriculture (USDA) contracts following revelations that JBS’s parent company pleaded guilty to charges of bribing Brazilian officials. For its crimes, JBS was made to pay the U.S. federal government a $256 million fine for its parent’s illicit bribery scheme. But Congressional Democrats understand that this supposed justice is undercut by the millions of dollars that JBS makes off the federal government every year in contracts. Since fiscal year 2019 alone, for example, more than $283 million in American public dollars has been ushered into JBS’s coffers. That amounts to nearly $30 million more than JBS’s fine. Democratic lawmakers, understandably, found this disparity to be reprehensible, prompting their outreach to Vilsack.

JBS has for years received millions of taxpayer dollars in bailout funds and contract awards. Those funds, from our tax dollars, have helped JBS become the largest meat producer in the world and the second largest global food company.

These huge public payouts have then been wielded by JBS (and other contractors like it) to monopolize USDA’s contracting system, creating a toxic cycle of dependency that cements contractors’ dominance in their given market. It is this dependency that led Vilsack, in a letter to Congress published by Politico, to declare that barring JBS “could hurt taxpayers because the company has so few competitors,” and that as a result USDA would continue to accept JBS bids in its contracting services.

Per The American Prospect, Vilsack himself is also unlikely to implement strict contractor ethic standards, given that he’s a “henchman of the very biggest agribusiness giants,” whose chief of staff went on to become a lobbyist at the very corporation in question. The impetus, therefore, must come from elsewhere.

There are many basic ethics reforms that could address these issues, like closing the revolving door between contractors and government agencies, preventing government awards from being used for stock buybacks and union busting, and enforcing strict standards of corporate eligibility for participation in contracting bids when other parts of the government sue for violations of federal law.

Such shifts in federal contracting rules would not only protect the public from corporate abuses, but would also advance the federal government’s financial interest.

Monopolists Dominate The Contracting Market

Alas, the government’s kids-glove treatment of JBS is far from novel. Across the federal landscape, agencies continue to contract with corporations found guilty of wrongdoing simply because those same companies have monopoly power in their given fields.

According to our research, in fiscal year 2022, the federal government gave over $48 billion in public funds to contractors that faced antitrust actions from the Department of Justice (DOJ) in 2021 or 2022. Federal agencies forked over an additional $48.6 billion of taxpayer money in fiscal year 2022 via contracts to firms that faced similar action or inquiry from the Federal Trade Commission (FTC) over monopoly behavior during that same period. All told, that’s just shy of $100 billion dollars that federal agencies have rewarded to corporations that were actively facing—or recently subject to—enforcement activity from other parts of the government for harmful (or illegal) monopoly conduct during 2022 alone.

To look at just the Pentagon, for example, one-third of Pentagon contracts since 2001 have been awarded to five hyper-consolidated companies: Lockheed Martin, Boeing, General Dynamics, Raytheon and Northrop Grumman. This lack of competition has “driv[en] up costs for the American taxpayer, degrad[ed federal] accountability infrastructures, and otherwise creat[ed] ‘Walmarts of War’” that hold hostage actual national security in favor of privatized profits. As the Revolving Door Project has explained, “the current [monopolistic] system also promotes the iniquitous pursuit of massive gains through ‘questionable or corrupt business practices that amount to waste, fraud, abuse, price-gouging [and] profiteering.’”

Monopolies and their prone-to-labor-abuse corporate models also hurt workers in the short term, hurt the taxpayer in the long-term, and have been found to deliver lower quality services in fulfillment of contracted work.

Last year, corporate profit margins in the United States reached their peak since 1950, as corporations padded their profits by raising prices under the pretext of rising costs, while actually fueling inflation. Meanwhile, American families suffered from runaway (and cruelly unnecessary) cost-of-living increases that have left more and more folks facing crises like homelessness and food insecurity.

While the corporate conniving fueling crippling inflation is occurring across economic sectors, it tends to be even more pronounced in highly concentrated industries with monopoly pricing power over crucial goods and services.

Monopolies are manifestly bad for consumers and they’re also bad for workers. Market consolidation leads to depressed household income and wage decreases; indeed, monopolies cost workers approximately 15-25 percent of their wages while charging the public more for less.

The Federal Government Should Be a Champion of Its Own Laws

Despite the selling power of contractors, the federal government wields significant buying power over contracted firms, as the government is the single biggest purchaser of goods and services in the world. The federal government oversees and distributes hundreds of billions of dollars to contractors each year, reaching nearly $700 billion in 2020 and $637 billion in 2021.

The sheer purchasing power of the federal government is unparalleled, leaving it with significant authority to implement and to enforce strict ethics standards for contractors. Despite this power, the government continues to casually fund JBS and other such companies’ grossly inflated profits (that hurt American consumers and families) and turned a blind eye to unlawful abuses of child labor and other workers, systemic underpayments of family farmers and ranchers, egregious food safety violations, and environmental crimes galore. Public money should not fuel the historic profit margins of corporations while those corporations hurt the public.

USDA and other large contracting agencies should be champions of the public good. They should reward contractors who do good work, and they should hold contractors accountable—and indeed stop fueling their government-sponsored bottom lines—when contractors violate federal law.

Instituting basic ethics in contracting is well within the executive branch authority and requires no action from Congress. From reevaluating what requires contractors in the first place to refusing to fund union-busting activities to refusing to promote monopolists, the contracting apparatus is fully within the purview of President Biden and his officers.

To address this crisis of competition and consolidation in contracting, this administration should bolster its existing executive order on competition by requiring executive agencies to provide a public report on the degree of competition (or lack thereof) that exists within their contracting apparatus. Biden could expand the purview of existing “advocates for competition,” to include identifying problems in federal procurement due to concentrated markets and charge. These officials could then be directed to collaborate proactively with the FTC and DOJ to actually and actively protect competition for their agency—a truly whole of government approach to competition.

Through instituting basic ethics and eligibility standards, federal agencies could foster actual competition in government contracting markets. Diversifying the deliverers of goods and services would yield greater accountability and good stewardship of public monies.

Toni Aguilar Rosenthal is a Researcher with the Revolving Door Project.

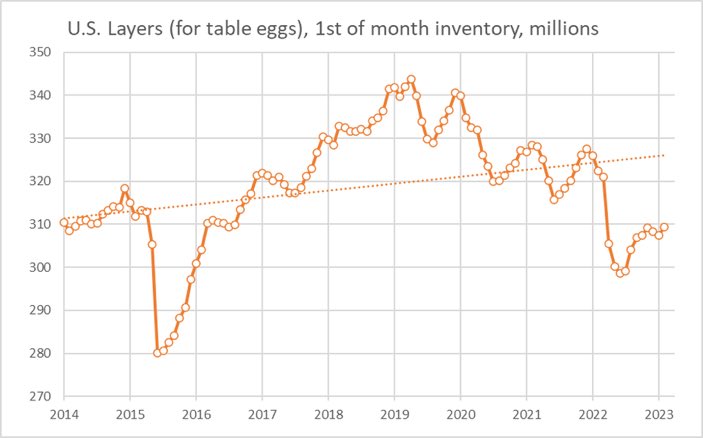

I love eggs. I really do. There was a year in law school where I religiously made and ate an egg sandwich for breakfast every day. To this day, I believe an egg fried in olive oil until the yolks are jammy and the edges are crispy is a perfect food.

Since last year, however, my egg-loving style has been cramped. As everyone knows, the price of eggs at the grocery store more than doubled in 2022, increasing from $1.78 a dozen in December 2021 to over $4.25 in December 2022. This 138-percent increase in egg prices far outstripped the 12-percent increase Americans saw in grocery prices generally over the same period. And some Americans have had it much worse, as average egg prices reached well over $6 a dozen in states ranging from Alabama to California and Florida to Nevada.

What’s behind the skyrocketing retail price of the incredible edible egg? Well, for one thing, the skyrocketing wholesale price of that egg. Between January 2022 and December 2022, wholesale egg prices went from 144 cents for a dozen Grade-A large eggs to 503 cents a dozen. This was the highest price ever recorded for wholesale eggs. Over the entire year, wholesale egg prices averaged 282.4 cents per dozen in 2022. When we consider that average retail egg prices for the same year were only about 3 cents higher at 285.7 cents per dozen, it becomes clear that the primary contributor to rising egg prices at the grocery store has been the dramatic increase in the wholesale prices charged by egg producers.

If this gives you hope that relief might be around the corner because you’ve heard something about a recent “collapse” in wholesale egg prices, sadly your hope would be misplaced. Despite this much-ballyhooed collapse, the average wholesale egg price has simply gone from 4-to-5 times what it was in January of last year to 2-to-3 times that number. If that weren’t enough, prices are expected to spike again when egg demand picks up in the run-up to Easter. Ultimately, the USDA is projecting that the average wholesale egg price in 2023 will be 207 cents a dozen—or only about 25% lower than the average price for 2022. So much for a collapse.

Are you wondering who sets these wholesale prices? Why, an oligopoly, of course. The production of eggs in America is dominated by a handful of companies led by Cal-Maine Foods. With nearly 47 million egg-laying hens, Cal-Maine controls approximately 20% of the national egg supply and dwarfs its nearest competitor. The leading firms in the industry have a history of engaging in “cartelistic conspiracies” to limit production, split markets, and increase prices for consumers. In fact, a jury found such a conspiracy existed as recently as 2018, and a wide-ranging lawsuit was brought just a couple of years ago accusing several of the largest egg producers (including Cal-Maine) of colluding to increase prices during the COVID-19 pandemic.

When asked about the multiplying price of their product, these dominant egg producers and their industry association, the American Egg Board, have insisted it’s entirely outside their control; an avian flu outbreak and the rising cost of things like feed and fuel, they say, caused egg prices to rise all on their own in 2022. And, sure enough, those were real headaches for the egg industry last year—about 43 million egg-laying hens were lost due to bird flu through December 2022, and input costs for producers certainly increased over 2021 levels. As my organization, Farm Action, detailed in letters to federal antitrust enforcers last month, however, the math behind those explanations for the steep increase in wholesale egg prices just doesn’t add up.

The reality, we argued, is that wholesale egg prices didn’t triple in 2022, and aren’t projected to stay elevated through 2023, because of “supply chain, ‘act of God’ type stuff,” as one industry executive has tried to spin it. Rather, the true driver of record egg prices has been simple profiteering, and more fundamentally, the anti-competitive market structures that enable the largest egg producers in the country to engage in such profiteering with impunity.

Is it really just profiteering? Yes, it’s really just profiteering.

According to the industry’s leading firms, rising egg prices should be blamed on two things: avian flu and input costs. We can stipulate for the sake of argument that, if a massive amount of egg production and, hence, potential revenue were lost due to avian flu, the largest producers would be justified in trying to recoup some of that lost revenue by raising prices on their remaining sales. Likewise, if there were a sharp rise in egg production costs, we can stipulate that producers would be justified in trying to pass them on to wholesale customers. But was there a nosedive in egg production? Did the cost of egg inputs multiply dramatically? Short answer: No, and No.

The bottom line on the avian flu outbreak is that it simply did not have a substantial effect on egg production. Although about 43 million egg-laying hens were lost due to avian flu in 2022, they weren’t all lost at once, and there were always over 300 million other hens alive and kicking to lay eggs for America. The monthly size of the nation’s flock of egg-laying hens in 2022 was, on average, only 4.8 percent smaller on a year-over-year basis. If that isn’t enough, the effect of losing those hens on production was itself blunted by “record high” lay rates throughout the year, which were, on average, 1.7 percent higher than the lay rate observed between 2017 and 2021. With substantially the same number of hens laying eggs faster than ever, the industry’s total egg production in 2022 was—wait for it—only 2.98 percent lower than it was in 2021.

Turning to input costs, it’s true they were higher in 2022 than in 2021, but they weren’t that much higher. Farm production costs at Cal-Maine Foods—the only egg producer that publishes financial data as a publicly traded company—increased by approximately 20 percent between 2021 and 2022. Their total cost of sales went up by a little over 40 percent. At the same time, Cal-Maine produced roughly the same number of eggs in 2022 as it did in 2021. If we take Cal-Maine Foods as the “bellwether” for the industry’s largest firms, we can be pretty sure that the dominant egg producers didn’t experience anywhere near enough inflation in egg production costs to account for the three-fold increase in wholesale egg prices.

Against the backdrop of these facts, the industry’s narrative simply crumbles. It’s clear that neither rising input costs nor a drop in production due to avian flu has been the primary contributor to skyrocketing egg prices. What has been the primary contributor, you ask? Profits. Lots and lots of profits.

Gross profits at Cal-Maine Foods, for example, increased in lockstep with rising egg prices through every quarter of the last year. They went from nearly $92 million in the quarter ending on February 26, 2022, to approximately $195 million in the quarter ending on May 28, 2022, to more than $217 million in the quarter ending on August 27, 2022, to just under $318 million in the quarter ending on November 26, 2022. The company’s gross margins likewise increased steadily, from a little over 19 percent in the first quarter of 2022 (a 45 percent year-over-year increase) to nearly 40 percent in the last quarter of 2022 (a 345 percent year-over-year increase).

The most telling data point, however, is this: For the 26-week period ending on November 26, 2022—in other words, for the six months following the height of the avian flu outbreak in March and April—Cal-Maine reported a five-fold increase in its gross margin and a ten-fold increase in its gross profits compared to the same period in 2021. Considering the number of eggs Cal-Maine sold during this period was roughly the same in 2022 as it was in 2021, it follows that essentially all of this profit expansion came from—you guessed it—higher prices.

But is this an antitrust problem? Yes, it’s an antitrust problem.

On their own, these numbers plainly show that dominant egg producers have been gouging Americans, using the cover of inflation and avian flu to extract profit margins as high as 40 percent on a dozen loose eggs.

Some agriculture economists and market analysts, however, have questioned whether this price gouging should raise antitrust concerns. The dramatic escalation in egg prices over the past year, they’ve argued, has just been “normal economics” at work. Per Angel Rubio, a senior analyst at the industry’s go-to market research firm, Urner Barry, the runaway increase in wholesale egg prices was simply a function of the “compounding effect” of “avian flu outbreaks month after month after month.” These outbreaks repeatedly disrupted egg deliveries, he presumes, driving customers to assent to spiraling price demands from alternative suppliers. In a blog post on Urner Barry’s website, Mr. Rubio further hypothesized that jittery customers may have “increased their ‘normal’ purchase levels to secure more supply,” goosing up prices even higher.

There are several reasons to doubt this theory of the case. To begin with, Mr. Rubio’s analysis presumes that avian flu outbreaks caused significant disruptions in the supply of eggs even though, as discussed above, the aggregate production data suggests that was not the case. But let’s assume that there were supply disruptions, and that these disruptions did lead to a glut of demand for reliable suppliers, giving them pricing power. If that were the case, it would stand to reason that Cal-Maine—which did not report a single case of avian flu at any of its facilities in 2022—had an opportunity to sell a whole lot more eggs in 2022 than in 2021, and to sell them at record-high profit margins. But Cal-Maine didn’t sell a whole lot more eggs. It sold roughly the same number of eggs. If Mr. Rubio’s theory were right, why did Cal-Maine leave money on the table?

Once we start applying this question to the pricing and production behavior of the egg industry’s dominant firms more broadly, a whole variety of competition red flags start cropping up

The red flags—they multiply!

Let’s talk about pricing first. In a truly competitive market, one would have expected rival egg producers to respond to a near-tripling of average market prices with efforts to undercut Cal-Maine’s skyrocketing profit margin and capture market share. Alas, that did not happen. In researching Farm Action’s letter to antitrust enforcers, we found no evidence of aggressive price competition for business among the largest egg producers. Yet everything about the mechanics of egg sales suggests that they should be competitive. Wholesale customers generally buy their eggs directly from producers. Long-term or exclusive contracts for egg supplies are rare. And the price of eggs in each purchase is individually negotiated. In other words, for each delivery of eggs they need, a wholesale customer is in all likelihood free to shop around and give rival suppliers an opportunity to undercut their incumbent supplier. Given this fluid sales environment, how did Cal-Maine manage to raise prices so much that its profit margin quintupled in one year without any other major producer coming to eat its lunch?

Another head-scratcher has been how the industry has managed to throttle production in the face of sustained high egg prices. As early as August of last year, the USDA was observing that favorable conditions existed, both in terms of moderating input costs and record-high egg prices, for producers to invest in expanding their egg-laying flocks. Yet such investment never materialized.

Even as prices reached unprecedented levels between October and December of last year, the number of eggs in incubators and the number of egg-laying chicks hatched by upstream hatcheries both remained flat, and were even below 2021 levels in December. As the year drew to a close, the USDA observed that “producers—despite the record-high wholesale price—are taking a cautious approach to expanding production in the near term.” The following month, it pared down its table-egg production forecast for the entirety of 2023—while raising its forecast of wholesale egg prices for every quarter of the coming year—on account of “the industry’s [persisting] cautious approach to expanding production.”