After years of inflation-driven concerns over the state of the economy, it seems that the mythical soft landing has been achieved; things aren’t perfect but inflation is down without the United States hitting a recession. The labor market has weakened some in recent months, but is still largely okay and the Federal Reserve has started cutting rates in a move to ease downward pressure on employment. In 2022, Bloomberg Economics put the odds of a recession within the next year at 100 percent. Two years later and not only has there not been a recession, but inflation is down, interest rates are going down, and recent GDP growth has been higher than it was for the previous decade.

Over the last several months, while this situation was crystalizing, many have credited Federal Reserve Chair Jerome Powell with achieving the once-mythical soft landing. That’s a mistake. There are multiple reasons why the Fed has been ineffective at best at wielding monetary policy in its recent inflation fighting. Such an explanation doesn’t fit the available empirics—or its advocates’ own model of how interest rates work.

The issue is especially salient because many of Powell’s defenders, including neoliberal economists and pundits, cling to the view that inflation was driven by demand-side factors. This spending-is-to-blame philosophy conveniently exonerates businesses for having any role in driving inflation. If demand-side explanations can be excluded, then attention would shift back to supply-based theories of inflation, including price gouging and coordinated price increases. And that would lead to very different policy implications.

A Brief History Lesson

Let’s rewind to when the fight over monetary policy was heating up in 2022. A variety of different economic shocks have hit the United States: the worst pandemic in a century, major emergency stimulus, brittle supply chains, and a land war in Europe (between Russia—one of the world’s major oil producers—and Ukraine—one of its major grain producers) have all rocked markets in just two years. Then, corporations in concentrated markets seize on the pricing mayhem to pad profits, extending inflationary pressures. At this point, such rent-seeking is well documented. That includes work from researchers from at least three regional Federal Reserve Banks (Boston, San Francisco, and Kansas City), the Bank of Canada, the International Monetary Fund, and the European Central Bank.

Because of this suite of shocks, inflation spiked more aggressively than it had for decades. That spike prompted the Fed to begin a major series of interest rate hikes to attempt to rein in price increases. This whole time there’s a back and forth among economists and pundits on what caused inflation, how long it would last, and what to do about it.

On one side you had Team Transitory, who said that the cause was a bunch of exogenous shocks, inflation wouldn’t last all that long, and we should wait things out because inflation will naturally subside and using monetary policy risked hurting workers.

On the other was what I called Team Crash The Economy, who said that the cause of inflation was fiscal stimulus leading to excess spending, price growth wouldn’t return to normal on its own, and the Fed should aggressively hike interest rates to cool the economy—including destroying millions of jobs. Larry Summers infamously called for ten percent unemployment while lounging on a beach.

In retrospect, Team Transitory was largely correct about the causes; fiscal stimulus played a role, but wasn’t responsible for most of inflation. Technically, Team Crash The Economy was right on the timeframe question, but the reasoning behind why inflation lasted a long time was demonstrably incorrect. Conversely, Team Transitory was technically wrong about the timeframe, but the reasoning was at least partially true.

But then there’s the big question of what the solution was. Both teams have taken victory laps: Team Transitory back in 2023 when inflation eased, except for a few lagging variables (housing, wages) and commodities (oil) that kept overall measures high; and Team Crash The Economy over the summer, when they pointed at decreased inflation and credited Jerome Powell and the Fed for the result.

The Econ 101 Model

The intro macro model for the relationship between inflation and interest rates is largely just an inverse relationship. As interest rates are eased, businesses face cheaper borrowing costs, inducing them to scale up operations, creating new jobs. Then when the labor market tightens, it creates a “wage-price spiral.” As people get paid more, they spend more, leading suppliers to scale up again, further tightening the labor market, leading to higher wages, and on and on. In this econ 101 telling, the key link between inflation and interest rates is those pesky workers demanding higher wages, which create a cycle of increasing demand. That’s why the solution is a form of “demand destruction,” forcing consumers to consume less (by making credit more expensive) in order to reduce demand-side pressure on prices.

So if a central bank finds itself making monetary policy using this framework in an inflationary environment, what does it do? It hikes rates, making borrowing costs prohibitively high, which leads firms to stop expanding and, if the costs increase enough, to actually shrink their business via measures like layoffs, putting an end to wage increases, or even shuttering entirely. And then as wages stagnate (or, in extreme cases, decrease), there’s less demand, so prices don’t continue their rapid increase (or, in extreme cases, fall).

Within the econ 101 frame, this makes sense and is the obvious choice. But in the real world, it didn’t fight inflation. Nearly every step of that theoretical model can be observed and empirics clearly do not show the proscribed pattern. On top of that, there are blatant theoretical holes in that narrative.

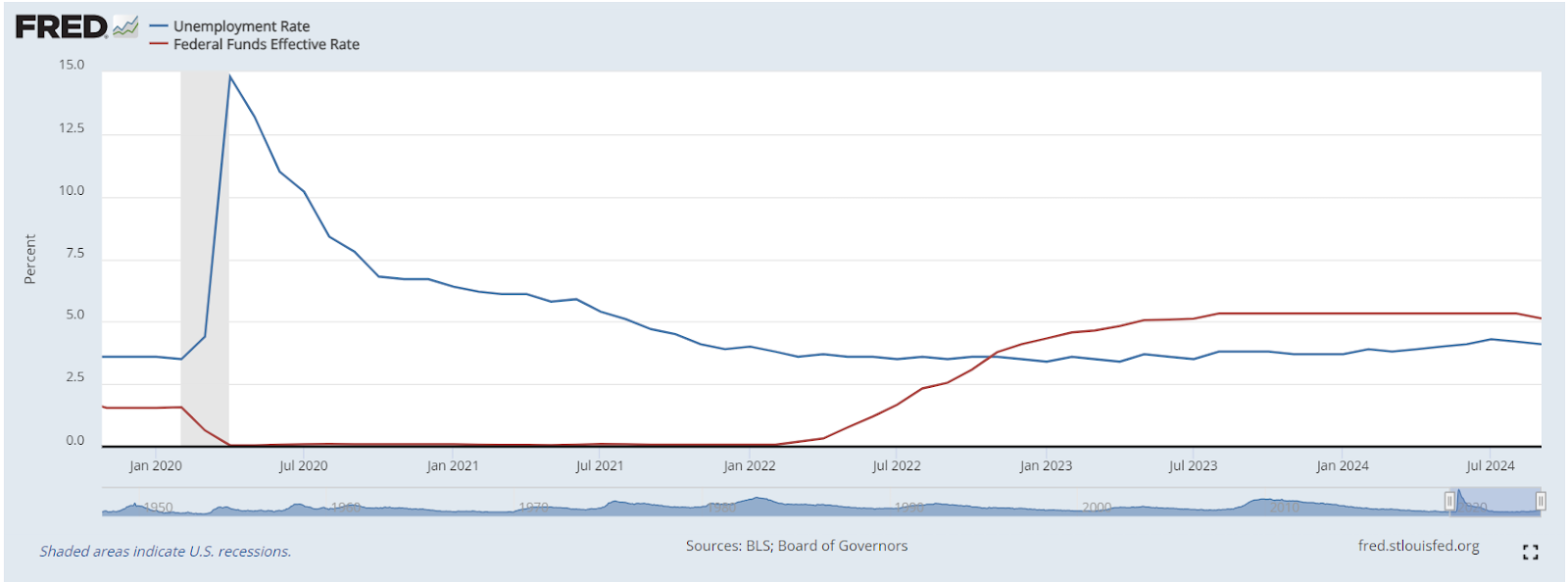

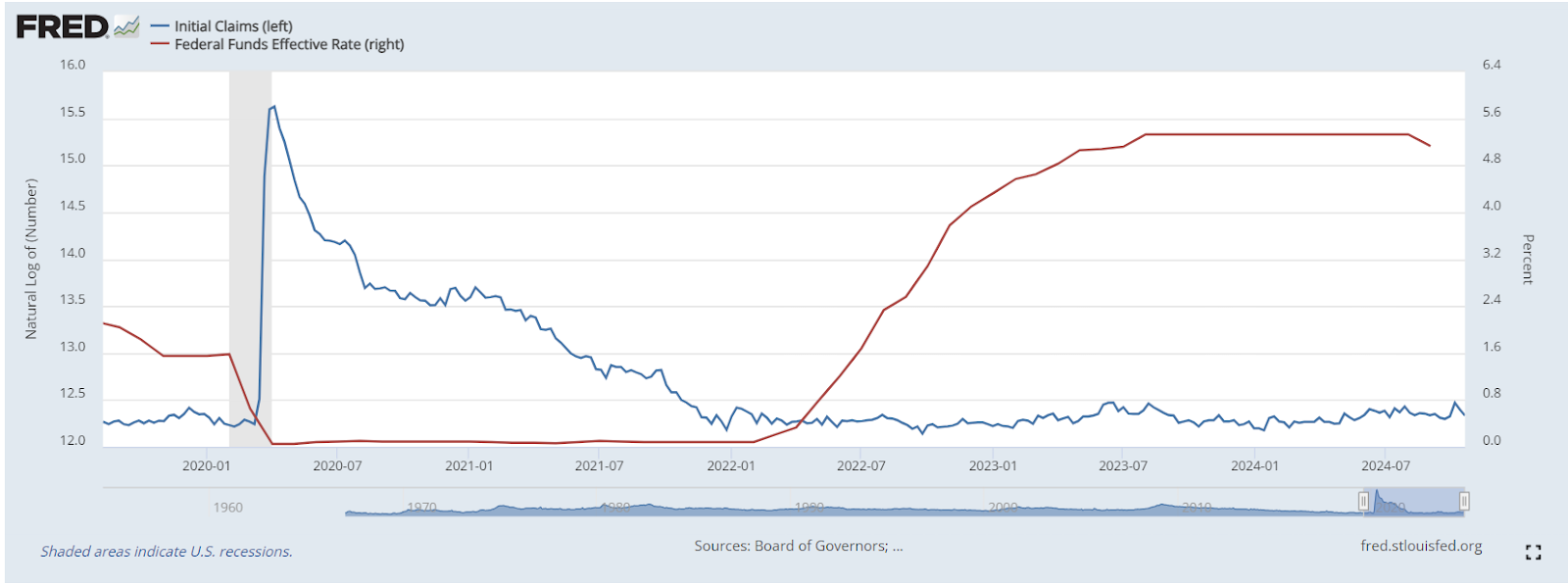

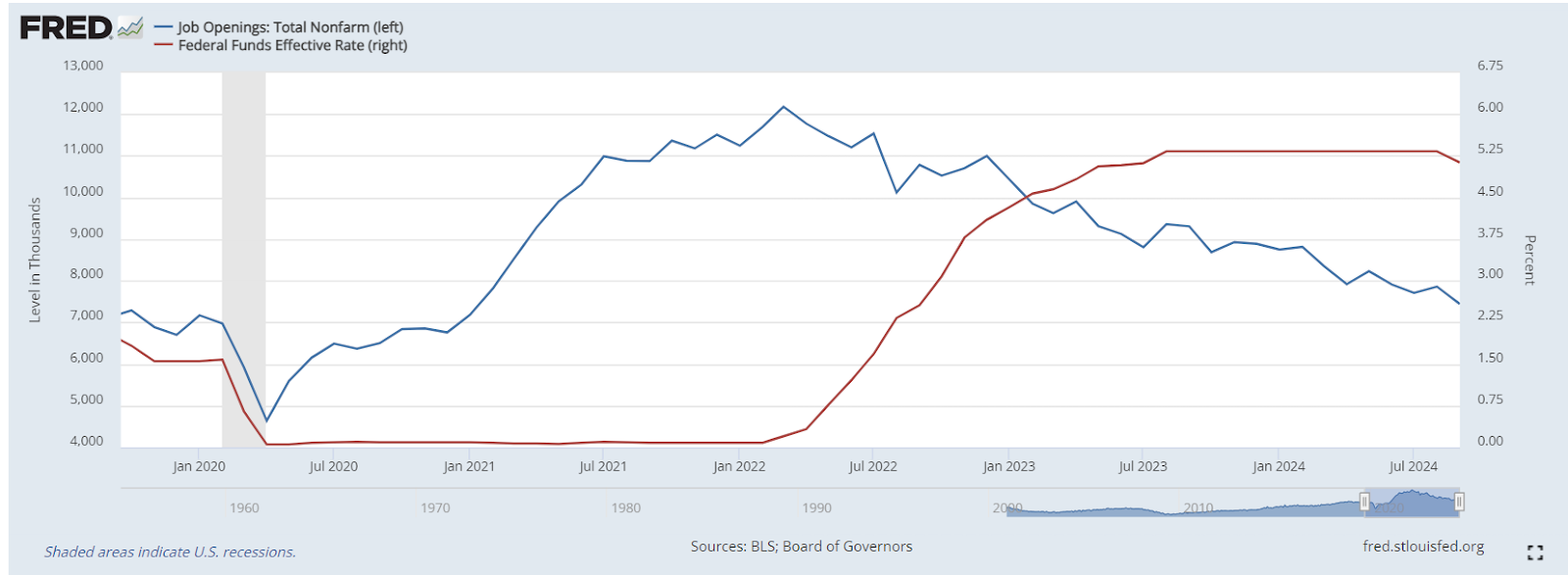

Let’s start with unemployment as the key channel to impact inflation. If the textbook econ 101 model is correct, we should be able to see it in a few different datasets. The unemployment rate (Figure 1) should go up as the Fed began raising rates in March 2022, and should correspond to a rise in initial filings for unemployment insurance (Figure 2) and a fall in job vacancies (Figure 3) and new job creation (Figure 3(a)).

Figure 1: Unemployment rate (blue, left) and effective federal funds rate (red, left) vs. date.

Figure 2: Initial unemployment insurance claims (blue, left) and effective fed funds rate (red, right) vs. date

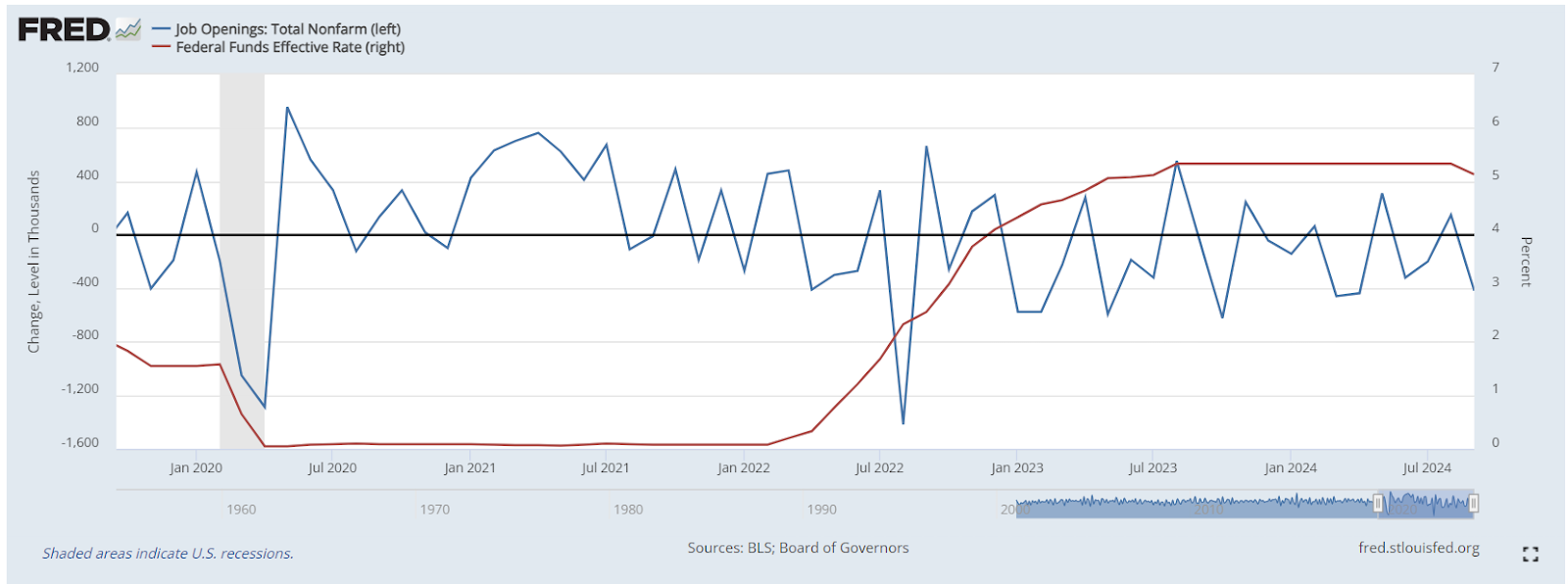

Only one of those trends is borne out by the data. Job openings have declined, and the monthly change (Figure 3(a)) has been lower recently. It’s worth noting, however, that the number of job openings is still historically high, above anything pre-pandemic. Plus demand destruction requires a decrease in real spending power, which a change in job openings alone won’t do.

Figure 3: Total job openings (blue, left) and effective federal funds rate (red, right) vs. date.

Figure 3(a): Monthly change in job openings (blue, left) and effective fed funds rate (red, right) vs. date.

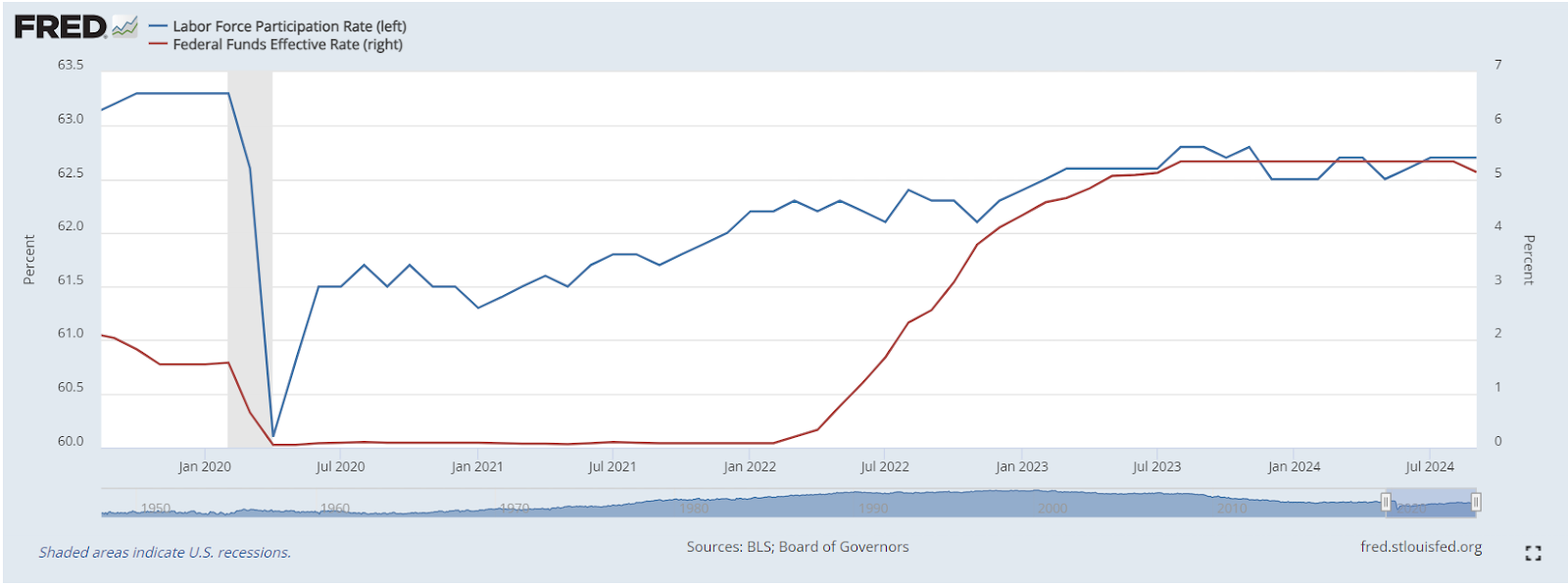

No dice. But maybe what happened is that work prospects got bad and that led a lot of people to exit the labor force entirely. Except that didn’t happen either. The labor force participation rate (Figure 4) has remained below 2019 levels, but reached its post-pandemic relative maximum of 62.8 percent in August 2023, the month at the end of the Fed’s rate hikes, and remained steady since.

Figure 4: Labor force participation rate (blue, left) and effective fed funds rate (red, right) vs. date.

Now let’s expand the intro model a little bit to see if there are factors that could be a viable channel to get from rate hikes to a fall in inflation. When the Fed increases rates, there are a bunch of things that should be expected to happen as a result of higher borrowing costs:

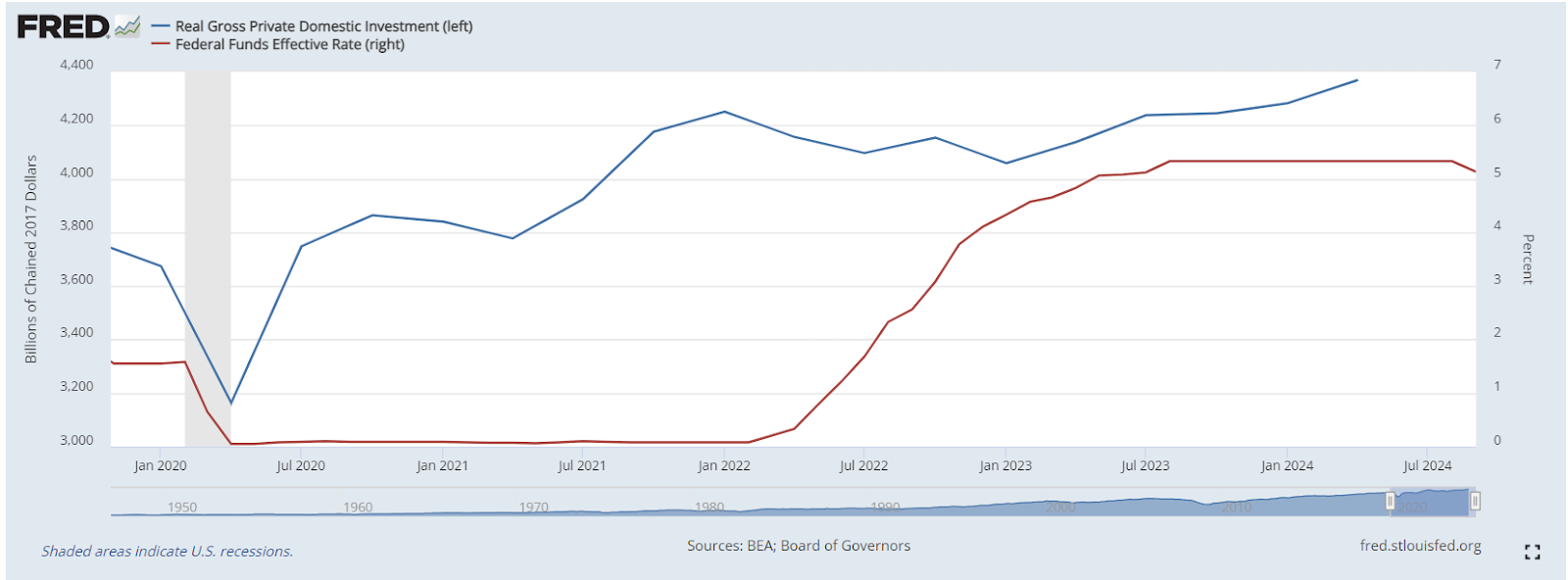

- Private investment (Figure 5) should fall, reflecting firms being unable to afford expanding with less access to credit.

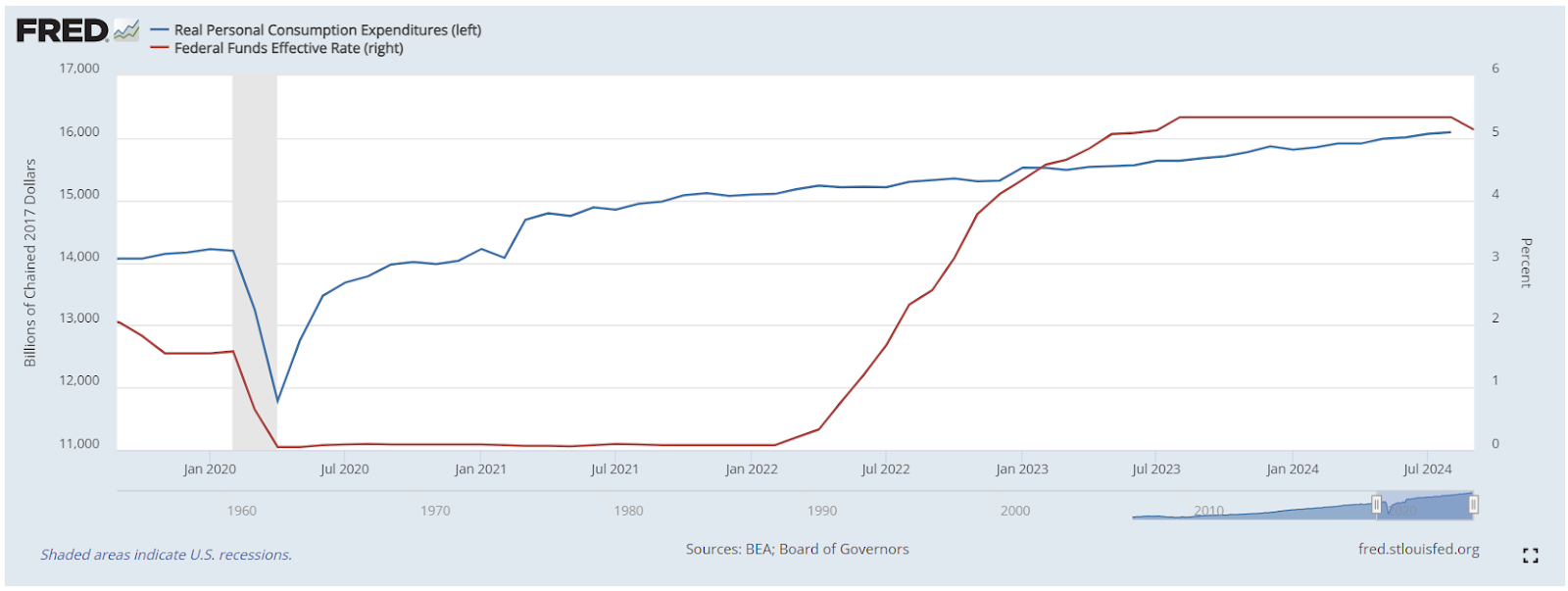

- Consumer expenditures (Figure 6) should fall, reflecting their lines of credit (including personal loans, mortgages, car loans, and credit cards) costing more to use and wage growth slowing.

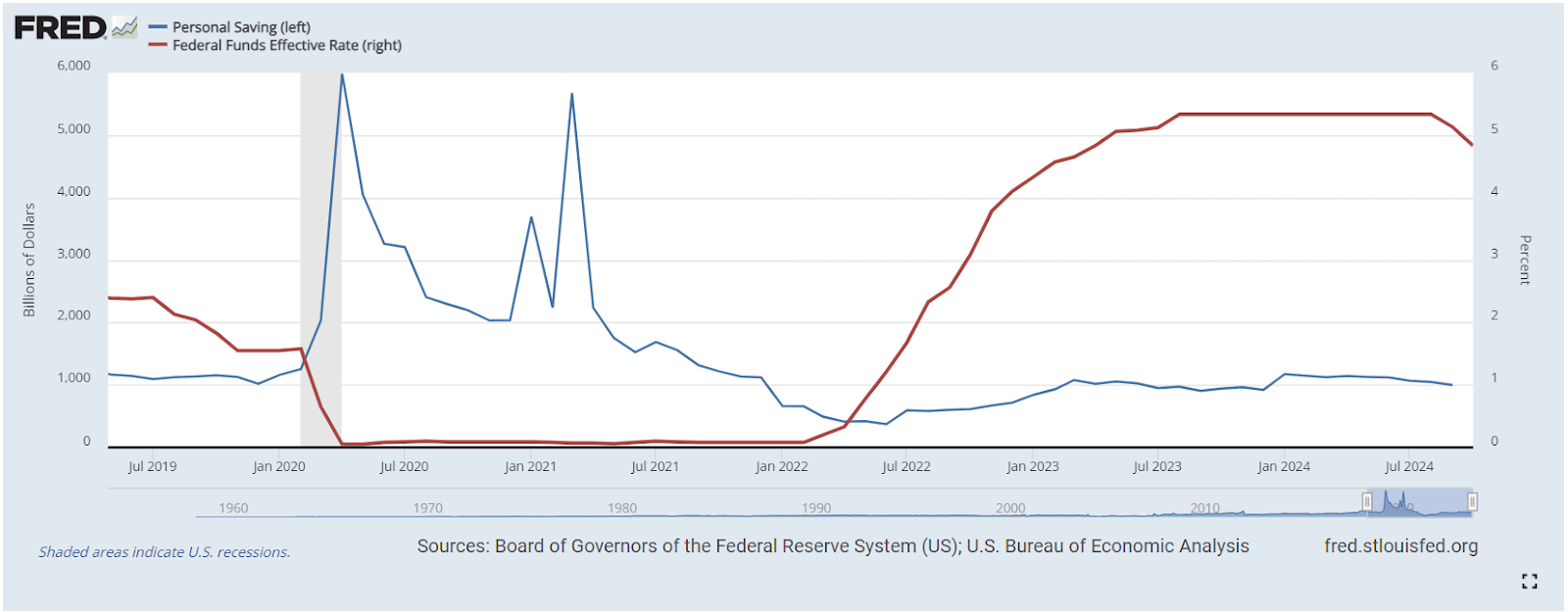

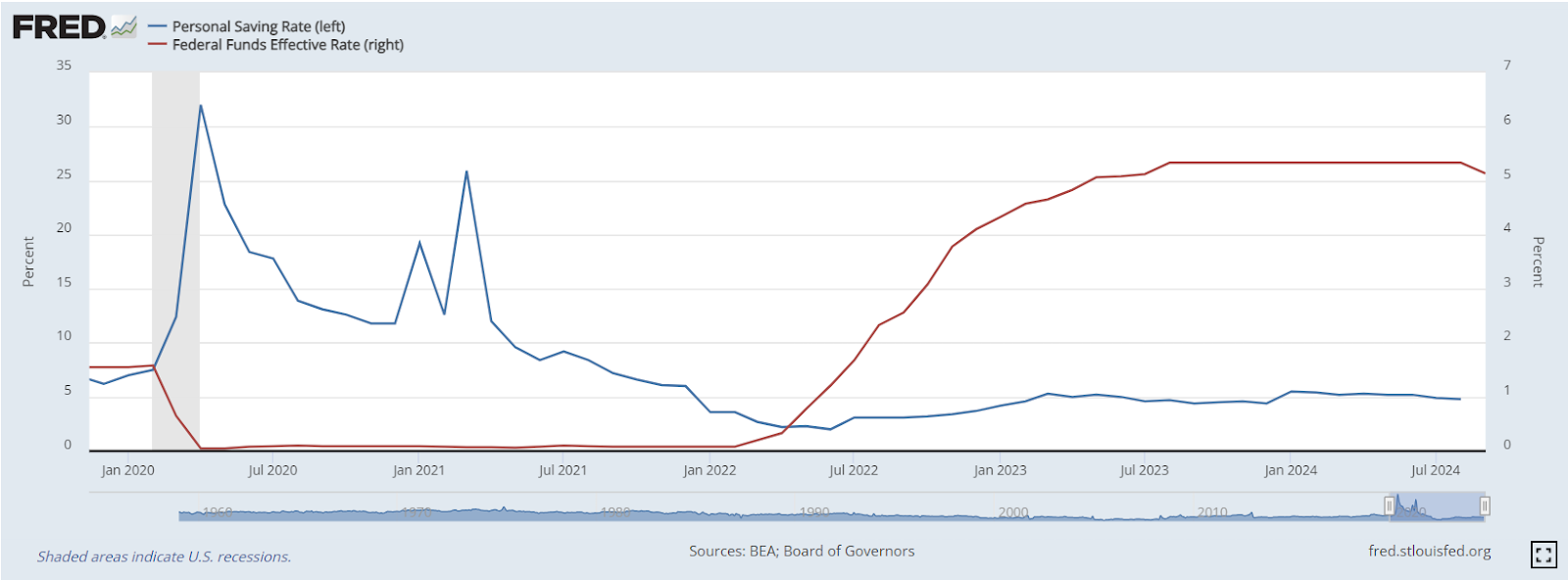

- Personal savings (Figure 7) should decrease as people eat into savings as a substitute for consumer credit. The savings rate (Figure 8) should fall, as more personal income is diverted directly to consumption to cover for using less credit.

Any of these could potentially be a mechanism for monetary policy to lower aggregate demand.

Figure 5: Real gross private investment (blue, left) and effective fed funds (red, right) vs. date.

Figure 6: Real consumption expenditures (blue, left) and effective fed funds rate (red, right) vs. date.

Figure 7: Personal Savings in nominal billions of dollars (blue, left) and effective fed funds rate (red, right) vs. date

Figure 8: Personal savings rate (blue, left) and effective fed funds rate (red, right) vs. date.

Yet exactly none of those causes are reflected in the data. (Total personal savings looks at first glance like it dipped, but it actually increased and stabilized during the course of the rate hikes.) If demand destruction does occur, it would presumably be through some combination of those factors. If there’s no loss of jobs, no drop in investment or consumption, and no change in personal savings rates, how exactly does increasing interest rates lead to lower inflation?

The short answer, at least in this case, is that it probably didn’t. This entire model of monetary policy presupposes demand-side causes of price increases, which were only a minority of the post-Covid inflation.

Inflation Doesn’t Capture the Full Cost of Living

That isn’t to say that the Fed’s rate hikes did nothing to impact workers and consumers. They actually made things worse. One long standing debate from the past couple of years is why public sentiment has remained negative on the economy even as most indicators have been broadly positive. A big part of that sentiment gap can be explained by differences in how lay people and economists use the same word. In an everyday sense, “inflation” means a rise in cost of living. But in economics, “inflation” is a change in the price level of a fixed basket of goods compared across time. That creates tension in how we discuss inflation; it’s atechnical measure that is often used in a general sense.

That meaning gap wouldn’t be a huge issue if the technical measure was a consistently good proxy for how people experience changes in the cost of living. There are prices that are important to the cost of living, however, that are excluded from the basket used to measure inflation. Chief among them is the cost of borrowing.

From a mechanical point of view, excluding interest rates on consumer credit is very reasonable; if they were to be left in, then it would muddle the relationship between interest rates and inflation since inflation would be defined as a function of interest rates. While it makes sense for technical economic analysis, this exclusion makes measures of inflation a poor approximation of the actual situation people experience.

Consumers experience higher interest rates on their access to credit as a sort of inflation. After all, it makes their lives more expensive. As a result, people’s lives can get more costly even in the face of easing inflation. (Not to mention that lower inflation still doesn’t represent a drop in prices.)

Put everything together and you get a story that goes something like this: multiple shocks, mostly, though not entirely, stemming from disruptions to supply usher in a major episode of inflation. As supply constraints eased, inflation fell. Although not before many unscrupulous firms took advantage of the situation by raising prices by more than their costs increased.

Meanwhile, neoliberal economists like Jason Furman and Larry Summers publicly pressured the Fed into hiking rates in an attempt to elevate unemployment and usher in demand destruction. Jerome Powell and the Fed ultimately did so, which made consumer credit more expensive, in turn that kept consumer confidence low because even though inflation was easing, it didn’t feel like it. Through those higher borrowing costs, the Fed has been responsible for eroding consumer confidence, threatening democracy, and slowing the green energy transition.

Yet what the data indicate is that these trends happened in parallel; over similar timeframes but not with a causal relationship between them. The expected changes to unemployment, investment, consumption, and personal saving are all missing. Absent those channels, there isn’t a link that gets from higher interest rates to lower inflation. It’s entirely possible that there is a causal channel somewhere, but until it’s identified and explicated, there is no reason to defer to the econ 101 model.

Particularly given the stink that neoclassical economists made about evidence for sellers’ inflation, they should be held to a similar standard for their crediting of the Fed for lower inflation and implicitly putting the blame on consumers and workers. The data just don’t fit their model.